Is Commercial Real Estate the latest canary in the economic coal mine?

According to recent economic data, sales of commercial mortgage bonds have fallen off a cliff, plummeting about 85% year-over-year as commercial real estate investors are bracing for what looks like a wave of defaults throughout the commercial real estate industry.

According to a recent Bloomberg News report, the collapse of the American mall industry could be right around the corner, and may cause a wave of commercial real estate defaults that extends to office spaces hit by the work-from-home scam.

Last year saw a 10% drop in commercial real estate loans — the underlying debt that typically gets repackaged into commercial mortgage bonds — compared to the year before, to $804 million from $891 million, according to Mortgage Bankers Association data. In addition, the trade group expects a further 15% drop in CRE loans in 2023 to $684 million, again slashing the number of loans that can be securitized and sold.

According to Fox News:

The giant investment manager Brookfield Asset Management recently defaulted on a total of over $750 million in debt for a pair of 52-story towers in Los Angeles, according to a February securities filing. Real-estate firm RXR is in talks with creditors to restructure debt on 61 Broadway, a 34-story tower in Manhattan’s financial district, according to people familiar with the matter. Handing over the building to the lender is among the options under consideration, these people said.

In another sign of distress, a venture of an investment manager affiliated with Related Cos. and BentallGreenOak is in similar debt-restructuring talks over a $150 million warehouse-to-office conversion project in Long Island City, N.Y., that hasn’t filled up as much space as expected, according to people familiar with the matter.

“Default risk has increased and could be more problematic if rates increase and the economy slows,” said Chris Sullivan, chief investment officer at United Nations Federal Credit Union. “So, I think a cautious and especially diligent approach is appropriate.”

So What does this mean for you?

For small business owners, the news is devastating and the trickle effect will eventually make it down to everyone. Thanks in large part to a generation of COVID workers who refuse to go back to work, small brick-and-mortar businesses are in real trouble. In fact, in Manhattan, for example, remote work is costing merchants $12.4 billion a year as workers no longer buy their morning coffees or get their dry-cleaning done in the city.

Are we living in fantasy land?

The United States faces a default sometime this summer or early fall if Congress does not raise or suspend the debt ceiling, a Washington think tank warned on Wednesday. But, as we reported late last year, it’s hard to see how we get out of this disaster unscathed. The federal government is essentially bankrupt and has entered the land of make-believe accounting.

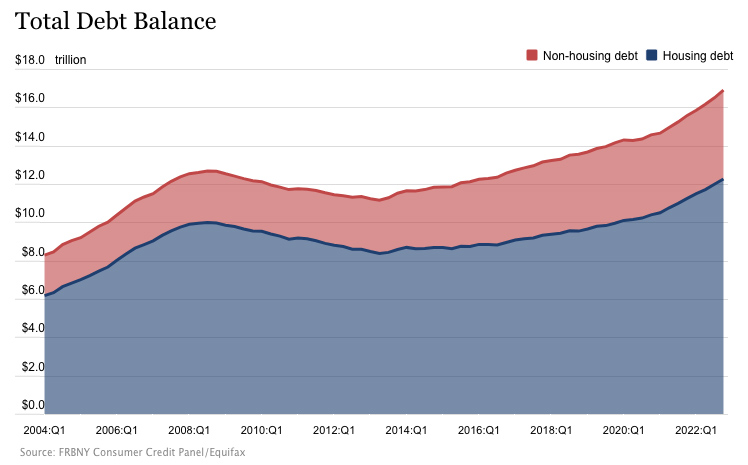

According to CNBC’s latest poll, the average American isn’t doing much better than our government. According to the latest New York Fed Household Debt and Credit report, total household debt rose by $394 billion in the last quarter of 2022. It was the most significant quarter-on-quarter rise in two decades.

Total household debt increased by 8.5% in 2022 and now stands at a record $16.9 trillion. That’s $2.75 trillion higher than it was pre-pandemic.

Credit card balances increased by another $61 billion in Q4.

In a recent podcast, Peter Schiff said the surge in credit card debt really evidences the fact that we don’t have a strong labor market.

If the labor market was really so strong, people’s paychecks would be high enough that they wouldn’t need to use credit to buy the things that they needed. They could actually afford to buy stuff without going deeper into debt, especially since interest rates are rising so much. You would think consumers would be reluctant to take on more debt in a rising rate environment. The only reason they’re doing it is because they really have no choice.”

Even more troubling, 64% of Americans say they are living paycheck to paycheck. Can you imagine what is going to happen when people realize there is no way off this sinking ship?

Preparing for an economic collapse

If you’re not prepared, you need to start taking steps to protect yourself and your family from future troubles.

Keep an eye on the markets, and keep an eye on the banks.

Before depositing any money in a bank, you need to research the financial soundness of that bank. Since the so-called end of the financial crisis, when the government spent over 700 billion dollars to “fix the system,” over 511 banks have failed.

With so many banks still going under, you really have to wonder how long the FDIC can continue to pay out on these insured deposits. With banking industry assets sitting at around $22.7 trillion, there is little reason to believe the FDIC can cover these insured deposits during a full-scale collapse.

While many believe the FDIC protects their money, the simple truth is, there’s not enough money to protect everyone. If the system collapses, your FDIC-insured account is anything but certain.

Realize your dollars may become worthless.

Over the last year, our money has become worth less and less by the month. From gas prices that have more than doubled in the last couple of years to soaring food prices and sky-high interest rates, our dollar is already becoming less valuable.

It would be best if you seriously looked at the possibility of an all-out collapse of the system. If this were to happen, your dollars would quickly become worthless.

You must start to take a balanced approach to being financially prepared for the future. While investing in your financial future is important, the same can be said for investing in your ability to survive future disasters. If you haven’t started preparing for economic troubles, now is the time to seriously consider stocking up to survive future financial problems.

Be Prepared to Defend Yourself

- Situational Awareness: How to Protect Yourself by Developing your Situational Awareness

- 7 Rules of Self Defense

- Self Defense: Defending yourself from multiple attackers

- Improvised Weapons: Self-defense in the Real World

- The Ultimate Situational Survival Guide: Self-Reliance Strategies for a Dangerous World

Investing in long-term consumable goods.

This means stocking up on items you will need and use in the future or stocking items you can barter with in case the system fails. By stocking up on food, water, survival gear & supplies, and bartering goods, you will have a nice stockpile of supplies that will help you through almost any disaster.

Another upside to investing in consumable goods is these goods are completely secure from financial market volatility and will continue to hold their value after the collapse. In fact, as we’ve seen over the last year, most consumables will probably skyrocket in value in a post-collapse world.

Be Prepared to Feed Yourself when the Collapse Hits!

- Best Emergency Food: The Top Survival Food Supplies

- Survival Food – 56 Long-Term Survival Foods and Supplies at the Grocery Store

- Prepper 101: Your Survival Guide to Getting Started

Grocery Options that ship right to your Home:

Learn to Be Self-sufficient NOW!

To truly be prepared, you need to learn how to be 100% self-sufficient.

- 30+ Self-Reliant Resources: Preparedness Skills that Everyone Should Know

- Urban Resources: Finding Food & Water During a Long-term Disaster

- Survival Fishing: Top Tips for Finding Fish during a Long-term Survival Situation

- Off Grid Living: A Real-world Guide to Going Off the Grid

- Homeschool: Taking your Child’s Education Off The Grid!

{kind=link}